|

|

|

|

The start of a new year always compels people to take a fresh look at their goals, from health and career to relationships and finance. But with historically low mortgage rates, increased home sales and price growth, and a tight housing inventory, the time is right to also make some homeownership resolutions for 2021.

Home buyers, is this the year you work to improve your credit score, pay down some debt, or save for a down payment? Home sellers, we’ve laid out plans for you to get top dollar for your property, including timing your home sale, making your property stand out from the crowd, and investing in your extra living space. And even if you’re staying put for awhile, homeowners, you can resolve to improve your status quo by evaluating your home budget, finalizing your home maintenance schedule, or maybe investing in a second property. So no matter your homeownership status, we’ve got some ideas and advice for you to make this year your best one yet. Read on to learn more. HOME BUYERS Resolution #1: Qualify for a better mortgage with a higher credit score. Your credit report highlights your current debt, bill-paying history, and other key financial information. Importantly for your home-buying journey, it is also used by lenders and companies to calculate your credit score, which partly determines if you are qualified to obtain a mortgage. Therefore, before you start house-hunting, make sure your finances are in the best possible shape by checking your credit report from Equifax, Experian, and TransUnion (via AnnualCreditReport.com). You can also obtain your credit score for free from some banks and credit card companies. Your credit score will be a number ranging from 300-850.1 Generally speaking, a credit score of 740 or higher is considered very good to excellent.2 If your FICO score drops below 740, you might need to work at boosting your score for a few months before you begin house-hunting. Ways to do this are to pay your bills on time every month, keep your credit card balances low, and avoid applying for new credit. Resolution #2: Improve your credit health by paying down debt. Do you have student loans, credit card debt, or car payments tying up your income each month? That debt is hurting your “buying power,” or the amount of home you can afford. Not only is it money that you can't spend on your new home, but your debt-to-income ratio also affects your credit score, which we discussed above. The less debt you have, the higher your FICO score and the better mortgage you can obtain. If you can, pay off some debt in its entirety--like a low balance on a credit card. Then apply that "extra" money you previously paid on that credit card to pay off bigger debt, like a car loan. Even if you can’t pay off all (or any) of your debt in full, reducing the balances of each account will help you qualify for the best possible mortgage terms. Resolution #3: Create a financial safety net before applying for a mortgage. Don’t forget that buying a home requires some cash as well. A down payment is typically 10-20% of a home’s purchase price, and closing costs currently average 2 to 3 percent of a home's purchase price.3,4 You’ll also need money for moving expenses and any initial maintenance tasks that might pop up. And as the pandemic taught us, you never know when an unforeseen event might cause a job loss, drop in income, or health scare, so having some liquid savings will ensure that you can still pay your mortgage if a crisis occurs. Dedicate some effort to building up your reserves. Cut down on unnecessary expenses, and consider having a portion of each paycheck automatically deposited into your savings account to avoid the temptation to spend it. HOME SELLERS Resolution #4: Decide on the right time to sell your home. If you’re looking to maximize profit on the sale of your home, selling earlier in the year makes sense. Listing prices historically increase early in the year, peak in May, plateau through June, and decrease for the remainder of the year.5 And, according to the National Association of Realtors, “[w]ith both mortgage rates and the number of homes available for sale expected to remain relatively low, home prices are likely to continue to increase. [In] mid-January, home prices typically begin a quick ramp-up in a normal year.”5 But sales price isn’t the only thing to consider. You might not be ready to sell your home yet because you don't want to uproot your kids during the school year or because you need to tackle some minor upgrades before placing your home on the market. This means that there is no one month or season that is the perfect time to sell your home. Instead, the right timeline for you takes into account factors such as when you’ll earn the highest profit, personal convenience, and whether your home is even ready to put on the market. A trusted real estate professional can talk you through your specific needs to clarify when to sell your home. Resolution #5: Boost your home’s resale value by making your property shine. Housing inventory is at historic lows across the country, and that means the market is fiercely competitive.6 Selling your home in 2021 has the potential to net you a huge return right now, and you can maximize that amount with some simple fixes to make sure your property outshines your neighbors' for sale down the street. In your home, you might need to tackle a minor remodeling project, such as upgrading the flooring or adding a fresh coat of paint. According to the National Association of Realtors’ 2019 Remodeling Impact Report, simply refinishing existing hardwood floors recoups 100% of the cost at resale, and completely replacing it with new wood flooring recovers 106% of costs.7 Outside, you might consider improving your curb appeal by removing a dead bush, trimming a tree that blocks the front window, or power-washing your moldy driveway and sidewalks. In fact, real estate agents say cleaning the exterior of your house can add $10,000 to $15,000 to a home’s sale price.8 And according to a Virginia Tech study, improving a home’s landscaping may increase its value by 10 to 12%.9 A good agent should provide custom-tailored suggestions to ensure your property pops inside and out. Ask us about our local insider secrets that will make your home stand out from others on the market. Resolution #6: Invest in your “extra” living space to meet current buyers’ needs. Due to COVID-19, more people are staying at home to work, go to school, exercise, and stay entertained. And these lifestyle changes are showing up in home buyer preferences. For example, according to one study, buyers are looking more and more for homes with formal, outfitted home offices, private outdoor spaces, and updated kitchen appliances.10 So if you’ve got an underutilized room, consider turning it into an office, home gym, schoolroom, or multi-purpose room to meet current home buyer needs and attract better offers on your home. Got some underwhelming space outside? You could turn it into an outdoor entertainment area by adding a firepit, upgrading the patio furniture, or installing a grilling area. Be sure to consult with a local real estate professional before investing in a renovation, however, as each market’s buyers have different tastes. HOMEOWNERS Resolution #7: Evaluate your household budget to reflect financial changes. After this past year, in particular, your financial picture may have changed. Maybe you were furloughed, had your hours reduced, or got a new job further from home. Perhaps you’ve kept the same job, but you’re now working remotely. A work-from-home arrangement could mean less money spent on gas, tolls, a professional wardrobe, and dining out for lunch. But this could also mean new (or increased) expenses now that you’re working at home, such as new tech-related purchases, faster Wi-Fi, and higher energy bills. January marks the perfect opportunity to update your income and expenses and review last year’s spending habits, tweaking as needed for 2021. For more specific ideas, check out this link "20 Ways to Save Money and Stretch Your Household Budget." Or just shoot us an email at [email protected]. Resolution #8: Save money now (and earn more later) with a home maintenance plan. Having a schedule of regular home maintenance projects to tackle will save you money now and in the long-term. You’ll avoid some surprise “emergency fixes,” and when you’re ready to eventually sell your home, you’ll get higher offers from buyers who aren’t put off by overdue repairs. Even if nothing necessarily needs fixing right now, you can lower your energy costs by maintaining and upgrading your home. According to the U.S. Department of Energy, simple fixes add up: replace five most frequently used bulbs with ENERGY STAR ones to save $75/year; repair leaky faucets to save $35/year; replace older toilets with low-flow models to save $100/year; and seal air leaks to save $83-$166/year.11 For a breakdown of home maintenance projects to tackle throughout the year, shoot me an email at [email protected] and I'll send you “House Care Calendar: A Seasonal Guide to Maintaining Your Home.” Resolution #9: Invest in real estate for a better standard of living. Even if you don’t plan on leaving your current residence, real estate is a great way to improve your quality of life in 2021. Have cabin fever from the long quarantine? A vacation home in a getaway location you love lets you safely spread your wings. And if you have been looking for a second stream of income, an investment property might be your answer. Just be sure to consult with a real estate professional to get a realistic sense of a property’s true income potential. Want more information on how a second property fits into your 2021 plans? Request our free report, "Move Up vs Second Home: Which One Is Right For You?" Just shoot us an email at [email protected]. LET US HELP YOU WITH YOUR 2021 GOALS Without a plan and a support system, 55% of Americans will break their new year’s resolutions.12 Whether you’re looking to buy, sell, or stay put in your home, it helps to connect with a trusted real estate agent to keep you motivated and on track. As local market experts, we have the knowledge, experience, and networks to help you achieve your homeownership goals, whatever they may be. Reach out to us today for a free consultation and commit to a happy and prosperous new year. Sources:

0 Comments

This year has demonstrated, perhaps more than ever, the importance of our family, friends, neighbors, and community. It truly “takes a village” to keep a community functioning effectively, whether that’s by keeping our waterways clean, feeding the hungry, teaching our kids, or supporting small businesses.

With the holidays right around the corner, December offers the perfect opportunity to give back to the place we call home. You might want to focus your efforts near home, expand to our larger community, or even help support the people closest to you. Whether you’re passionate about a particular cause or just want to get more involved in general, let these 10 ways, both big and small, inspire you to do good in your town. GIVE BACK NEAR HOME 1. Attract local wildlife. By making your neighborhood more wildlife friendly, you’re helping to create a balanced and healthy ecosystem. Plus, many of the animals you can attract help with pest control and pollination.1 Ideas:

Take action: While you might not be able to “break ground” until spring, start researching native plants now to design a landscaping plan that provides food, shelter, and water for local wildlife. 2. Clean up our community. Besides beautifying the area, picking up trash keeps it out of our local waterways, which means a cleaner water supply for all of us. Ideas:

Take action: Check with your local municipality to learn about environmental clean-up efforts in our community, as well as recycling and composting. 3. Organize or join a neighborhood watch. According to a recent report, neighborhoods with Neighborhood Crime Watch programs experience roughly 16 percent less crime.3 Keeping an eye out for each other instills a sense of safety and security in your neighborhood by increasing surveillance, reducing opportunities, and enhancing information sharing among residents. Even if your neighborhood doesn’t have an official program, you can still share crime information via a neighborhood Facebook group or apps like NextDoor. Ideas:

Take action: Some police forces use online mapping tools that provide crime alerts to people in neighborhoods where recent criminal activity occurred.3 Share this information with your neighbors. HELP OUT LOCAL ORGANIZATIONS 4. Boost your civic engagement. Regardless of your politics, you can get more involved as a citizen to make a positive difference in our community. Ideas:

Take action: Do you know who our local leaders are, such as our mayor or city councilwoman? Get to know their names, their policies, and their stand on issues that affect our community. Subscribe to their newsletter and follow them on social media. 5. Support local businesses. Our community has been impacted by the pandemic, with many businesses being forced to limit capacity, instill social distancing efforts, and even shutter entirely in some cases. Help keep money in our local economy by shopping local instead of relying on online shopping from national chains. Ideas:

Take action: If you’re concerned about shopping in person right now, many of these businesses, though small, offer online shopping, with options for in-store pick-up, curbside delivery, and/or mail options. 6. Donate to local charities. Nonprofits could always use your financial support, so consider making a monetary donation to help them carry out their mission in our community. But if money is tight (or you want to support in other ways), think beyond just donating dollars. Ideas:

Take action: Many collection efforts run by charitable organizations and businesses take place during the holidays. Look to see what’s already taking place in our community and choose one or more to give to this season. CARE FOR YOUR NEIGHBORS 7. Organize a holiday food drive. This year, in particular, people are struggling to pay their bills and put food on the table. The pandemic has caused many businesses to close or reduce their staff size, putting many people out of work. Ideas:

Take action: Take advantage of your grocery store coupons and buy-one-get-one offers to inexpensively stock up on nonperishable goods. 8. Adopt a family or an individual. The holidays can be a struggle, especially financially, for some families. They might not be able to buy a Christmas tree or presents for their children. Maybe their holiday meal consists of boxed macaroni and cheese because they can’t afford a turkey and fresh vegetables. You can make a difference by “adopting” a particular family (or even just a child) to help make their holiday special. Ideas:

Take action: This works great as a family project. Get the kids in your life involved to help make holiday cards and pick out toys to give to the children in the adopted family. 9. Volunteer. Depending on your schedule and your preferences, you might be able to volunteer in-person or from home, whether it’s a one-time effort or ongoing project. It’s a great way to meet like-minded people in your community as you make a positive impact together for a shared cause. Ideas:

Take action: Start with your local community to see where its needs are the greatest. Make a point to help this holiday season, perhaps extending your commitment throughout 2021. 10. Perform random acts of kindness. Don’t think you need to “go big or go home” in your give-back efforts. You can make a big difference one small act at a time. Ideas:

Take action: Need more ideas? Visit randomactsofkindness.org for hundreds of inspiring ways to make someone’s day a little brighter. HOW WE CAN HELP YOU? As real estate experts in our local community, we’re tuned into the unique needs of the place we all call home. Reach out to us today to discuss more ways to make a positive impact in our community—this holiday season and beyond. And we want to make sure you’re taken care of, too. If you’re thinking about buying or selling a home now or in the near future, let us help you! Sources:

“2020 will be known for a lot of things, and a record-breaking year for real estate will certainly be one of its more unexpected legacies,” prominent economist Daryl Fairweather said.1 And he’s right: most of us would have expected the housing market to suffer from circumstances like a once-in-a-hundred-years pandemic and historic inventory shortages.

But, rather than a slowdown, we are continuing to experience a surprisingly robust real estate market across the country. And experts estimate that these conditions are likely to last well into the new year. Fannie Mae Senior VP and Chief Economist Doug Duncan predicts that existing home sales will ultimately “be up a percent or more in 2021.” He believes home prices will continue to rise due to limited inventory, but he is confident the Federal Reserve will keep interest rates low into the future, which will be “very good for households.”2 Market conditions like fewer available listings, changing criteria for desired homes, and record-low mortgage rates are changing the way people buy and sell homes, most likely in a lasting way. But this sustained activity, even in the uncertainty that is 2020, proves that our country still views real estate as a sound investment. The only question now is how you can take advantage of the housing market’s “new normal.” FEWER LISTINGS EQUALS A SELLER’S MARKET Inventory, meaning the number of homes for sale, is at a record low across the country. The National Association of Realtors (NAR) reports there are fewer homes on the market today than the association has seen in data going all the way back to 1982.3 Currently, the total housing inventory is about 1.47 million units, which is a decline of 19.2% from one year ago.4 Experts do predict some relief on the horizon. MarketWatch had previously anticipated housing starts would occur at a pace of 1.45 million and building permits would come in at a pace of 1.52 million.5 But it turns out that the market exceeded expectations: compared with last year, housing starts are up 11% and permitting for new homes occurred at a seasonally-adjusted annual rate of 1.55 million. That represents a 5% increase from August and an 8% increase from a year ago. For now, the fact that there are fewer listings creates an advantageous housing market for sellers. There are several reasons why. For one, buyers have to act fast to snap up available homes. As a result, most properties that come on the market stay for an average of just 21 days before they are sold.6 “That is the fastest ever recorded in our monthly series,” says NAR Chief Economist Lawrence Yun. Another benefit is that sellers are enjoying higher net returns on their listings. This is thanks to the tough competition for homes, which often results in bidding wars between buyers. Nationwide, the median home price in September rose to $311,800. That translates to about $40,000 (15%) more than just a year ago.7 This seller’s market is not simply a product of the pandemic. In fact, in the country’s top 100 metro markets, inventory has been dwindling since the first quarter of 2020.8 This means that even with increased construction, buyers can’t simply wait for things to go back to normal before reentering the market. Rather, all signs indicate that this is the new normal. What It Means for Homeowners: These higher home prices show that buyers are willing to spend more on a home right now than they did last year. So, if there ever were a time to list for top dollar—and expect to receive asking price quickly—that time is now. Ask me for a free consultation of your home’s value today. What It Means for Homebuyers: Due to low inventory, buyers could easily find themselves in a bidding war. Time is of the essence in a seller’s market, so you’ll need to get your financing in order and be pre-approved for a loan before you begin your home search. I can connect you with a trusted mortgage professional to get you started. BUYERS BENEFIT FROM LOW MORTGAGE RATES AND A BIGGER PLAYING FIELD Don’t worry, homebuyers. This “new normal” of real estate has benefits for you too. For example, people used to base their next home purchase on how far the commute was to work or in which public school district it was. But now, thanks to the pandemic shifting the locus of jobs and work, they are free to consider what they need from a home to make it a place they truly want to be in as they work, teach, exercise, cook, and live. Often, this equates to needing more space in different types of areas. Realtor.com consumer surveys show that people are desiring quieter neighborhoods, home offices, updated kitchens, and access to the great outdoors.9 The search for these criteria is driving residents out of densely populated metropolitan areas and into the suburbs.10 And this exodus from cities is good news for buyers: it opens up more possibilities for inventory that they could not have considered pre-pandemic. Another advantage for buyers is the record-low mortgage rates. The average rate for a 30-year fixed-rate mortgage hit a record low in mid-October when rates fell to 2.81%. That’s the lowest since Freddie Mac began conducting the survey in 1971, and well below last year’s 3.69%.11 Similarly, a 15-year fixed-rate mortgage can be had for as low as 2.35% compared to 3.15% a year ago. Thanks to these rates, buyers are afforded the opportunity to buy nearly $32,000 more home than they could one year ago, while keeping their monthly payment the same.12 So even though home prices are high now, it is currently more affordable to buy a home now than it was last year. If you want to take advantage of these rock-bottom mortgage rates, you need to act fast. Though rates are projected to stay low, housing economists predict that the window of opportunity to get the best rate could be closing in the coming months. Mike Fratantoni, chief economist at the Mortgage Bankers Association, said he expects the average rate on a 30-year mortgage to rise to 3.5% by the end of 2021.13 What It Means for Homeowners: Record-low mortgage rates offer you the opportunity to lower your monthly payment—or even take out some equity—with a refinance. With those additional funds, you could even choose to invest in a second home in a new desirable location. Reach out to me for a referral to a trusted mortgage professional or an agent in those markets. What It Means for Homebuyers: The time is now to determine how much home you can comfortably afford and make a plan to find it. I can set up a search for you to find homes that best meet your new needs, even if they’re in neighborhoods you wouldn’t have considered before. A RECORD-SETTING YEAR FOR HOME SALES IS JUST THE BEGINNING Despite the seemingly adverse buyer conditions, 2020 experienced a 14-year high number of home sales, NAR reports. Existing-home sales, which include single-family homes, townhouses, condominiums and co-ops, rose 9.4% in September to a seasonally adjusted annual rate of 6.54 million.14 That’s a 21% increase from a year ago! Every region of the country has seen a surge in sales activity. According to George Ratiu, senior economist for Realtor.com, part of the reason for these continued sales is that the pandemic has created a paradigm shift in the patterns of real estate.15 For example, housing needs are typically resolved by late summer and early fall to coincide with the commencement of the new school year. With homeschooling and remote work, however, buyers have been freed to continue their home search into the traditionally slow winter months. Another reason for the robust market is that Millennials are finally putting their money into home-ownership. According to the U.S. Census Bureau, the home-ownership rate for 25-to-34-year-olds rose to 40.7% by the end of last year.16 This is significant because Millennials, the generation of people in their mid-20s to late-30s, currently surpasses Baby Boomers as the nation’s largest living adult generation. As the remaining percentage of this group starts investing in homes in the near future, demand will persist. All of these factors indicate that the housing market is poised to remain strong as we head into the new year. And as Jonathan Woloshin, head of U.S. real estate at UBS Global Wealth Management, believes, they could “buoy the housing market for years to come.”17 What It Means for Homeowners: It’s tempting to believe that homes will basically sell themselves in a market like this. But we’re still seeing properties that are overpriced and under-marketed sit unsold. We can help you optimize the process of selling your home so you can get the best possible offer. What It Means for Homebuyers: Preparation is key to success in a seller’s market like this, but don’t let yourself become paralyzed. We are here to answer your questions and offer sound advice to guide you through all the options that are available to you. REAL ESTATE IS A SAFE BET Your other investments might have been on roller coasters this year, but the real estate market has been steady, competitive, and strong throughout. That makes it a good choice for your financial future. National real estate numbers can give us a pulse on the market, but real estate happens in our own backyard. As your local market experts, we can help you understand the finer points of the market that impact sales and home values in your own neighborhood. If you’re considering buying or selling a home before the new year or in early 2021, contact me now to schedule a free consultation. I’ll work with you to develop an actionable plan to meet your goals. Sources:

For years now, virtual home tours have helped real estate buyers far and wide find the perfect home. From long-distance military personnel being relocated, to investors expanding their portfolio, to homeowners looking for a vacation getaway, this technology makes finding a house that’s a bit out of driving distance much easier. And for real estate agents, virtual tours have been a useful way to help buyers with their home search and to assist sellers in creatively marketing their listings.

Because of the pandemic, virtual home showing options recently experienced a huge spike in popularity. One survey found that nearly 33% of recent home tour requests were for virtual tours, as compared to just 2% pre-pandemic.1 And it’s easy to see why. Buyers want to quickly find their next safe haven, one that may need to serve as their office, gym, and even classroom for months to come. And sellers want to limit the number of strangers in their home, yet still have the ability to reach enough potential buyers to get the best offer on their property. Virtual home tours are the popular thing right now, but that doesn’t automatically mean they’re the only option for your home-buying or selling experience. In this post, we’ll reveal five important secrets behind the virtual real estate scene. Read on to learn how they impact today’s home buyers and sellers. SECRET #1: Virtual Tours Have Evolved Lots of real estate professionals who had never used virtual tours before were forced to quickly adapt when the pandemic struck. Because of restrictions on time and resources, not everyone is able to create what would have been deemed a “virtual tour” last year. So instead, we’ve expanded the definition of the phrase by creating innovative new ways to show homes while keeping our clients safe and socially-distanced. Here are some terms you might come across as you explore homes with virtual tours. Traditional virtual tours use 360° Photos, which are images that allow you to see all angles of a space. These are what allow virtual tour viewers to look up, down, and all around the interior and exterior shots of a home. Using a software program, 360° photos can be stitched together to create a digital model that looks like a dollhouse. This is called a 3D Tour. Sometimes agents will also add Virtual Staging, which decorates rooms with digital furniture and accents like wallpaper or paint. Traditional virtual tours allow you to click to move from room to room in the home, but Online Walk-throughs feature the actual action of walking around. Either the seller or the agent (depending on factors such as time and safety requirements) will create a video by holding their camera or smartphone and simply moving through the home. Online Walk-throughs can be filmed in advance or happen live. If they are live, they can also be referred to as Virtual Showings or Online Open Houses. A Virtual Showing is often a scheduled, one-on-one event that mimics an in-person tour of the home, in which the agent and viewer start at the exterior and move their way through the property. If your agent offers to FaceTime or Skype you from a home you’re interested in, for example, that would be a type of Virtual Showing. In contrast, an Online Open House is more freeform, allowing more viewers to pop in and out of a group video call on apps such as Facebook or Zoom. SECRET #2: Virtual Doesn’t Mean Impersonal All these styles of virtual tours showcase the property’s details better than static photos ever could. But for a purchase as intimate as your next home, details like a new refrigerator or the size of the master closet aren’t the only deciding factors. Luckily, virtual tours are exceptional tools for personal connection. As a prospective buyer, virtual tours give you a feel for the property, inside and out, so you can easily picture yourself in the space and decide if the home’s flow and features work for your lifestyle. Live video walk-throughs with the real estate agent will give you insights on those crucial non-visual aspects, like creaky floors, super-fast internet speed, and neighborhood dynamics. Plus, you’ll be able to ask questions and get an insider’s perspective on what’s so great about the home. For sellers, if your agent recommends using a virtual tour to market your home, you could attract more buyers.2 And you can be sure that those interested buyers are still getting the up-close and personal look inside your home that will inspire their strongest offers. SECRET #3: Virtual Is Just The First Step To Safe Home Sales Even as government restrictions begin to ease in some areas, virtual tours are still recommended as a safer way to buy and sell real estate.3 Buyers don’t have to worry about exposure to anyone who previously visited the property, and sellers cut down on the foot traffic in their home. Some data even suggest that virtual tours keep agents safer as well, since they’re hosting fewer in-person showings and open houses.4 But despite the variety of virtual tours available, some buyers will still need to visit a home themselves in order to feel confident enough to submit an offer. In this situation, listing agents and sellers will work together to come up with a procedure that ensures everyone feels safe and comfortable. Some recommendations include requiring interested buyers to present a pre-qualification letter, conducting tours only by appointment and with essential parties, and asking buyers to self-disclose whether they have COVID-19 or exhibit any symptoms.3 The day of the in-person tour, agents might ask buyers to remain in their vehicle until they arrive at the property, and to wear protective gear such as face coverings and gloves. Many will provide hand sanitizer and will ask buyers to refrain from touching any surfaces in the home. Instead, the agent (or seller, prior to the buyers’ arrival) will turn on lights, open doors, and pull back curtains. Then, after everyone has left, the agent will return the home to its original state and disinfect it as needed.3 SECRET #4: The Speed of Closing Depends on Your Goals Though maybe not literally, virtual tours are opening doors for both buyers and sellers in terms of options available to them. In 2019, buyers viewed an average of 10 homes over a period of 10 weeks before submitting an offer.5 But thanks to an increased prevalence of virtual tours saving them driving time, they’re able to peek inside that number of homes in a much shorter period to make their final choice. With all this viewing activity, it makes sense that sellers whose listings feature virtual tours are receiving more offers on their properties. According to one study, virtual tours can add between two and three percent to the sales price of a home, in part because increased buyer interest has made sellers feel confident waiting for the exact right offer.2 So if you’re a buyer luxuriating in viewing homes from your couch, just remember that you’re not alone in your search. Your competition is virtually viewing the same properties you are, so it’s still important to work with your real estate agent to quickly submit a strong offer when you find the home of your dreams. And for sellers, if a speedy sale is important to you, carefully weigh that against the temptation to entertain more and more offers, which can keep your home on the market up to six percent longer.2 Your agent can help you decide the right strategy for your priorities. SECRET #5: Virtual May Not Always Be the Right Choice Creating, editing, uploading, and marketing virtual tours for a listing can be pricey. Packages through popular 3D imaging platforms like Matterport and Immoviewers can cost hundreds of dollars on their own.6 Virtual staging will further bloat a listing’s marketing budget, and then there’s the advertising dollars needed. Even seemingly inexpensive options like video call walk-throughs still require time and energy on behalf of both the seller and agent. These costs mean that a full virtual tour package might not always be the right choice for sellers. When you talk to your agent about marketing your home, it may be that an elaborate virtual tour, showing, and open house just don’t make sense. It could be that your potential buyers may not resonate with that type of marketing, that the investment-to-return ratio isn’t in your favor, or that there are more effective ways to get your listing seen by qualified buyers. Buyers, you may notice that some listings within your search parameters don’t offer virtual tours. That’s because those for-sale homes might not have needed a full virtual marketing package to entice buyers to submit offers, or those homes are better marketed through more traditional tactics. Don’t close the door on your dream home because it doesn’t have virtual events and features. Stay open-minded so you can consider the wealth of home options that fit your lifestyle, needs, and budget. ARE VIRTUAL HOME TOURS IN YOUR FUTURE? As technology develops, it will become easier and cheaper to create virtual tours. Coupled with the high demand for them, this means that virtual tour options are likely not only here to stay, but will continue to grow into a common addition to listings. If buying or selling a home is on your mind, we’d be happy to discuss how virtual tours can play a part in your real estate experience. Reach out to me today for help finding local homes for sale that have virtual tours, or to chat about if adding a virtual tour to your upcoming listing is the right fit. Sources:

September is usually the time for children everywhere to head back to school. But as the coronavirus pandemic continues to upend various areas of life, countless schools are opting to resume classes via remote learning.

While this “new normal” can be challenging for parents and kids alike, remote learning also offers some opportunities that kids may not experience in the classroom. If your children are embarking on a new school year with remote learning, here are four tips that may help them get the most out of the experience:

Sources: education.jhu.edu   The pandemic has changed the way many of us live, work, and attend school—and those changes have impacted our priorities when it comes to choosing a home.

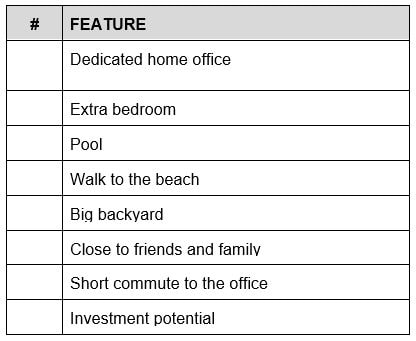

According to a recent survey by The Harris Poll, 75% of respondents who have begun working remotely would like to continue doing so—and 66% would consider moving if they no longer had to commute as often. Some of the top reasons were to gain a dedicated office space (31%), a larger home (30%), and more rooms overall (29%).1 And now that virtual school has become a reality for many families, that need for additional space has only intensified. A growing number of buyers are choosing homes further from town as they seek out more room and less congestion. In fact, a recent survey found that nearly 40% of urban dwellers had considered leaving the city because of the COVID-19 outbreak.2 But not everyone is permanently sold on suburban or rural life. Instead, some are choosing to purchase a second home as a co-primary residence or frequent getaway. Without the requirements of a five-day commute, many homeowners feel less tethered to their primary residence and are eager for a change of scenery after spending so much time at home. If you’re feeling cramped in your current space, you’ve probably considered a move. But what type of home would suit you best: a move-up home or a second home? Let’s explore each option to help you determine which one is right for you. WHY CHOOSE A MOVE-UP HOME? A move-up home is typically a larger or nicer home. It’s a great choice for families or individuals who simply need more space, a better location, or want features their current home doesn’t offer—like an inground pool, a different floor plan, or a dedicated home office. Most move-up buyers choose to sell their current home and use the proceeds as a down payment on their next one. If you’re struggling with a lack of functional or outdoor space in your current home, a move-up home can greatly improve your everyday life. And with mortgage rates at their lowest level in history, you may be surprised how much home you can afford to buy without increasing your monthly payment. 3,4 (To learn more about mortgage rates, contact us for a free copy of our recent report! “Lowest Mortgage Rates in History: What It Means for Homeowners and Buyers”) One major benefit of choosing a move-up home is that you can typically afford a nicer place if you spend your entire budget on one property. However, if you’re longing for that vacation vibe, a second home may be a better choice for you. WHY CHOOSE A SECOND HOME? Once reserved for the ultra-wealthy, second homes have become more mainstream. Home sales are surging in many resort and bedroom communities as city dwellers search for a place to escape the crowds and quarantine in comfort.5 And with air travel on hold for many families, some are channeling their vacation budgets into vacation homes that can be utilized throughout the year. A second home can also be a good option if you’re preparing for retirement. By purchasing your retirement home now, you can lock in a low interest rate, start paying down the mortgage, and begin enjoying the perks of retirement living while you’re still fit and active. Plus, it’s easier to qualify for a mortgage while you’re employed, although you may be charged a slightly higher interest rate than on a primary home loan. 6 One advantage of choosing a second home is that you can offset a portion of the costs—and in some cases turn a profit—by renting it out on a platform like Airbnb or Vrbo. However, be sure to consult with a real estate professional or rental management company to get a realistic sense of the property’s true income potential. WHICH ONE IS RIGHT FOR ME? You may read this and think: I’d really like both a move-up home AND a second home! But if you’re dealing with a limited budget (aren’t we all?), you’ll probably need to make a choice. These three tactics can help you decide which option is right for you. 1. Determine Your Time and Financial Budget You may meet the bank’s qualifications to purchase a home, but do you have the time, energy, and financial resources to maintain it? This is an important question to ask yourself, no matter what type of home you choose. Most buyers realize that a second home will mean double mortgages, utilities, taxes, and insurance. But consider all the extra time and expense that goes into maintaining two properties. Two lawns to mow. Two houses to clean. Two sets of systems and appliances that can malfunction. Second homes aren’t always a vacation. Make sure you’re prepared for the labor and carrying costs that go into maintaining another residence. Of course, some move-up homes require more work than a second home. For example, if your move-up option is a major fixer-upper, you’ll probably invest more energy and capital than you would on a small vacation condo by the beach. Have an honest discussion about how much time and money you want to spend on your new property. Would a move-up home or a second home be a better fit given your parameters? 2. Rank Your Priorities If you’re still undecided, make a wish list of the characteristics you’d like in your new home. Then rank each item from most to least important. This exercise can help you determine your “must-have” features—and which ones you may need to sacrifice or delay. Here’s a sample to help you get started: 3. Explore Your Options Once you’ve determined your parameters and priorities, it’s time to begin your home search. If you’re still not sure whether a move-up home or a second home is right for you, I can help. Contact me to schedule a free consultation. We’ll discuss your options and I'll help you assess the pros and cons of each, given your unique circumstances. We can also send you property listings for both move-up homes and second homes within your budget so you can better envision each scenario. Sometimes, viewing listings of homes that meet your criteria can make the decision clear. LET’S GET MOVING Whether you’re ready to make a move or need help weighing your options, I’d love to help. I can determine your current home’s value and show you local properties that fit within your budget. Or, if your heart is set on a second home in another market, I can refer you to an agent in your dream locale. Contact me today to schedule a free, no-obligation consultation! Sources:

When selling your home, you likely make it a priority to ensure that the front entrance and interior rooms shine. But as buyers in different price ranges and geographical areas increasingly value functional outdoor living spaces, it’s important to invest in your home’s exterior—whether you have a small patio, a sprawling yard, or anything in between.

As you get ready to showcase your home to potential buyers (even if you're not quite ready to sell yet - you'll still benefit by having an inviting place to spend time outside - especially these days), here are a few ideas for creating an enticing outdoor living space:

In July, the average 30-year fixed-rate mortgage fell below 3% for the first time in history.1 And while many Americans have rushed to take advantage of this unprecedented opportunity, others question the hype. Are today’s rates truly a bargain?

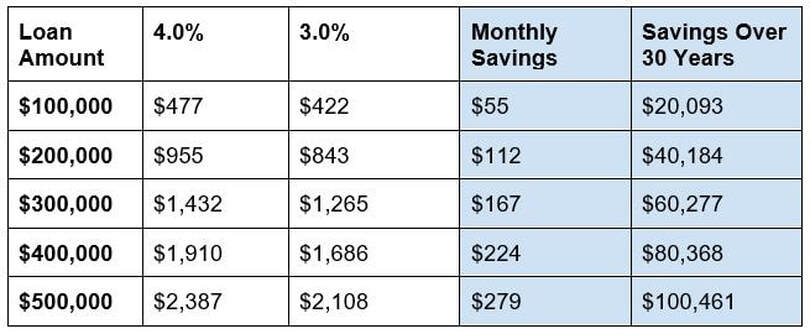

While average mortgage rates have drifted between 4% and 5% in recent years, they haven’t always been so low. Freddie Mac began tracking 30-year mortgage rates in 1971. At that time, the national average was 7.31%.2 As the rate of inflation started to rise in the mid-1970s, mortgage rates surged. It’s hard to imagine now, but the average U.S. mortgage rate reached a high of 18.63% in 1981.3 Fortunately for home buyers, inflation normalized by October 1982, which sent mortgage rates on a downward trajectory that would bring them as low as 3.31% in 2012.3 Since 2012, 30-year fixed rates have risen modestly, with the daily average climbing as high as 4.94% in 2018.4 So what’s causing today’s rates to sink to unprecedented lows? Economic uncertainty. Mortgage rates generally follow bond yields, because the majority of U.S. mortgages are packaged together and sold as bonds. As the coronavirus pandemic continues to dampen the economy and inject volatility into the stock market, a growing number of investors are shifting their money into low-risk bonds. Increased demand has driven bond yields—and mortgage rates—down.5 However, according to National Association of Realtors Chief Economist Lawrence Yun, “the number one driver of low mortgage rates is the accommodating Federal Reserve stance to keep interest rates low and to buy up mortgage-backed securities.” According to Yun, “we will see mortgage rates stay near this level for the next 18 months because of the significance of the Fed’s stance.”6 HOW DO LOW MORTGAGE RATES BENEFIT CURRENT HOMEOWNERS? Low mortgage rates increase buyer demand, which is good news for sellers. But what if you don’t have any plans to sell your home? Can current homeowners benefit from falling mortgage rates? Yes, they can! A growing number of homeowners are capitalizing on today’s rock-bottom rates by refinancing their existing mortgages. In fact, refinance applications have surged over the past few months—and for a good reason.7 Reduced interest rates can save homeowners a bundle on both monthly payments and total payments over the lifetime of a mortgage. The chart below illustrates the potential savings when you decrease your mortgage rate by just one percentage point. When it comes to refinancing, the bigger the spread, the greater the savings. Be sure to factor in any prepayment penalties on your current mortgage and closing costs for your new mortgage. For a refinance, expect to pay between 2% to 5% of your loan amount.8 You can divide your closing costs by your monthly savings to find out how long it will take to recoup your investment, or use an online refinance calculator. For a more precise calculation of your potential savings, we’d be happy to connect you with a mortgage professional in our network who can help you decide if refinancing is a good option for you. HOW DO LOW MORTGAGE RATES BENEFIT HOME BUYERS? We’ve already shown how low rates can save you money on your mortgage payments. But they can also give a boost to your budget by increasing your purchasing power. For example, imagine you have a budget of $1,500 to put toward your monthly mortgage payment. If you take out a 30-year mortgage at 5.0%, you can afford a loan of $279,000. Now let’s assume the mortgage rate falls to 4.0%. At that rate, you can afford to borrow $314,000 while still keeping the same $1,500 monthly payment. That’s a budget increase of $35,000! If the rate falls even further to 3.0%, you can afford to borrow $355,000 and still pay the same $1,500 each month. That’s $76,000 over your original budget! All because the interest rate fell by two percentage points. If you’ve been priced out of the market before, today’s low rates may put you in a better position to afford your dream home. On the other hand, rising mortgages rates will erode your purchasing power. Wait to buy, and you may have to settle for a smaller home in a less-desirable neighborhood. So if you’re planning to move, don’t miss out on the phenomenal discount you can get with today’s historically-low rates. HOW LOW COULD MORTGAGE RATES GO? No one can say with certainty how low mortgage rates will fall or when they will rise again. A lot will depend on the trajectory of the pandemic and subsequent economic impact. Forecasters at Freddie Mac and the Mortgage Bankers Association predict 30-year mortgage rates will average 3.2% and 3.5% respectively in 2021.9,10 However, economists at Fannie Mae expect them to dip even lower to an average of 2.8% next year.11 Still, many experts agree that those who wait to take advantage of these unprecedented rates could miss out on the deal of a lifetime. “With rates now at all-time historic lows, it’s hard to imagine that people may be holding out for something even better," warns Paul Buege, president and COO of Inlanta Mortgage.12 Positive news about a vaccine or a faster-than-expected economic recovery could send rates back up to pre-pandemic levels. HOW CAN I SECURE THE BEST AVAILABLE MORTGAGE RATE? While the average 30-year mortgage rate is hovering around 3%, you can do a quick search online and find advertised rates that are even lower. But these ultra-low mortgages are typically reserved for only prime borrowers. So what steps can you take to secure the lowest possible rate? 1. Consider a 15-Year Mortgage Term Lock in an even lower rate by opting for a 15-year mortgage. If you can afford the higher monthly payment, a shorter mortgage term can save you a bundle in interest, and you’ll pay off your home in half the time.13 2. Give Your Credit Score a Boost The economic downturn has made lenders more cautious. These days, you’ll probably need a credit score of at least 740 to secure their lowest rates.14 While there’s no fast fix for bad credit, you can take steps to help your score before you apply for a loan:15 ● Dispute inaccuracies on your credit report. ● Pay your bills on time, and catch up on any missed payments. ● Hold off on applying for new credit. ● Pay off debt, and keep balances low on your credit cards. ● Don’t close unused credit cards (unless they’re charging you an annual fee). 3. Make a Large Down Payment The more equity you have in a home, the less likely you are to default on your mortgage. That’s why lenders offer better rates to borrowers who make a sizable down payment. Plus, if you put down at least 20%, you can avoid paying for private mortgage insurance. 4. Pay for Points Discount points are fees paid to the mortgage company in exchange for a lower interest rate. At a cost of 1% of the loan amount, they aren’t cheap. But the investment can pay off over the long-term in interest savings. 5. Shop Around Rates, terms, and fees can vary widely amongst mortgage providers, so do your homework. Contact several lenders to find out which one is willing to offer you the best overall deal. But be sure to complete the process within 45 days—or else the credit inquiries by multiple mortgage companies could have a negative impact on your credit score.16 READY TO TAKE ADVANTAGE OF THE LOWEST MORTGAGE RATES IN HISTORY? Mortgage rates have never been this low. Don’t miss out on your chance to lock in a great rate on a new home or refinance your existing mortgage. Either way, we can help. We’d be happy to connect you with the most trusted mortgage professionals in our network. And if you’re ready to start shopping for a new home, we’d love to assist you with your search--all at no cost to you! Contact us today to schedule a free consultation. The above references an opinion and is for informational purposes only. It is not intended to be financial advice. Consult a financial professional for advice regarding your individual needs. Sources: 1. CNN Business - https://www.cnn.com/2020/07/16/success/30-year-mortgage-rates-record-low/index.html 2. Freddie Mac - http://www.freddiemac.com/pmms/pmms30.html) 3. Value Penguin - https://www.valuepenguin.com/mortgages/historical-mortgage-rates 4. Federal Reserve Bank of St. Louis - https://fred.stlouisfed.org/graph/?g=NUh 5. Bankrate - https://www.bankrate.com/mortgages/how-interest-rates-are-set/ 6. Washington Post - https://www.washingtonpost.com/business/2020/06/25/mortgage-rate-remains-historic-low/ 7. Yahoo! Finance - https://finance.yahoo.com/news/mortgage-refinancing-makes-big-comeback-151500346.html 8. Bankrate - https://www.bankrate.com/mortgages/is-no-closing-cost-for-you/ 9. Freddie Mac June 2020 Quarterly Forecast - http://www.freddiemac.com/fmac-resources/research/pdf/202006-Forecast.pdf 10. Mortgage Bankers Association Mortgage Market Forecast July 15, 2020 - https://www.mba.org/news-research-and-resources/research-and-economics/forecasts-and-commentary 11. Fannie Mae July 2020 Housing Forecast - https://www.fanniemae.com/resources/file/research/emma/pdf/Housing_Forecast_071420.pdf 12. Washington Post - https://www.washingtonpost.com/business/2020/06/25/mortgage-rate-remains-historic-low/ 13. Investopedia - https://www.investopedia.com/articles/personal-finance/042015/comparison-30year-vs-15year-mortgage.asp 14. Money - https://money.com/mortgage-rates-below-three-percent/ 15. Experian - https://www.experian.com/blogs/ask-experian/credit-education/improving-credit/improve-credit-score/ 16. Equifax - https://www.equifax.com/personal/education/credit/report/understanding-hard-inquiries-on-your-credit-report/  Whether you’re prepping your house to go on the market or looking for ways to maximize its long-term appreciation, these nine home improvement projects are great ways to add function, beauty, and real value to your home.

The best part is, once you’ve secured the materials, most of these renovations can be completed over the course of a weekend. And they don’t require a lot of specialized skills or experience. So grab your toolbox, then get ready to boost your home’s appeal AND investment potential! 1. Spruce Up Your Landscaping Landscaping improvements can increase a home’s value by 10-12%.1 But which outdoor features do buyers care about most? According to a survey of Realtors, a healthy lawn is at the top of their list. If your lawn is lacking, overseeding or laying new sod can be a worthwhile investment—with an expected return of 417% and 143% respectively.1 Planting flowers is another great way to enhance your home’s curb appeal. And if you choose a perennial variety, your blooms should return year after year. For an even longer-term impact, consider planting a tree. According to the Council of Tree and Landscape Appraisers, a mature tree can add up to $10,000 to the value of your home.2 2. Clean The Exterior When it comes to making your house shine, a sparkling facade can be just as important as a clean interior. Real estate professionals estimate that washing the outside of a house can add as much as $15,000 to its sales price.3 A rented pressure washer from your local home improvement store can help you remove built-up dirt and grime from your home’s exterior, walkway, and driveway. Just be sure to read the instructions carefully—and only use it on surfaces that can withstand the intensity. When in doubt, a scrub brush and bucket of sudsy water will often do the trick. 3. Add A Fresh Coat Of Paint New paint can have a big impact on both the appearance and value of a property. In fact, it’s one of the most effective ways to revitalize a home’s exterior, update its interior, and make it appear larger and brighter. The best part? Painting is relatively easy and inexpensive! To get the maximum return at resale, stick with a modern but neutral color palette that will appeal to a broad range of buyers. According to a recent survey of home design experts, cool neutrals are a safe bet when it comes to interior paint. And respondents chose white and gray as the best exterior paint colors to use when selling a home.4 However, it’s important to consider a property’s architecture, existing fixtures, and regional design preferences, as well. 4. Install Smart Home Technology In a recent survey, 78% of real estate professionals said their buyer clients were willing to pay more for a home with smart technology features.5 The most requested smart devices? Thermostats (77%), smoke detectors (75%), home security cameras (66%), and locks (63%).6 The good news is, many of these gadgets are fairly easy to install. And some of them, including smart thermostats and light bulbs, will pay for themselves over time by making your home more energy efficient. In fact, many manufacturers report that smart thermostats can cut back on heating and cooling costs by 10-20%.7 If you already own a smart speaker, like Amazon Alexa or Google Home, choose devices that will pair with your existing technology. This will enable you to create a truly integrated (and in many cases voice-activated) smart home experience. 5. Modernize Your Window Treatments Smart—or motorized—blinds are also growing in popularity, and several manufacturers make models you can order and install on your own. But they’re not the only way to modernize your window treatments. If you have old aluminum blinds, consider replacing them with plantation shutters, which are energy efficient, durable, and have strong buyer appeal.8 Roman and roller shades are another stylish alternative, and they come in a variety of colors and fabrics, which you can personalize to meet your design and privacy preferences. Fortunately, upgrading your blinds has gotten easier and less expensive in recent years. There are a number of retailers that specialize in affordable window coverings that are simple to measure and hang yourself. 6. Replace Outdated Fixtures Drastically transform the look and feel of your home by swapping out dingy and dated fixtures for contemporary alternatives. Start by assessing your current light fixtures, faucets, cabinet hardware, door knobs, and even switch plates. Then prioritize replacing those that are particularly outdated or in highly-visible areas, such as your entryway or kitchen. Even if your home is fairly new, consider trading your builder-grade fixtures for higher-end options to give it a more upscale appearance. And forget the old rule about sticking to one metal tone throughout your property. According to designers, mixing metal finishes can add interest and character to a space.9 For more designer insights and decor trends, contact me for a free copy of my recent report: “Top 5 Home Design Trends for a New Decade.” 7. Upgrade Your Bathroom Mirror A minor bathroom remodel offers one of the best returns on investment, with a $1.71 increase in home value for every $1 you spend.10 We’ve already explored several improvements you can make to your bathroom: new paint, fixtures, and hardware. Now complete the look by upgrading your vanity’s mirror. Before you purchase a new mirror, examine your existing one to see how it is attached to the wall. Some vanity mirrors are glued to the wall and difficult to remove without shattering the glass or damaging the sheetrock behind it.11 If you prefer to keep your existing mirror, you can paint the frame—or add one if it’s currently frameless. There are several online retailers that will send you the frame components cut to your specifications, which you can assemble and mount yourself. Much like a work of art, your vanity mirror serves as a focal point for your bathroom, so let your creativity shine through! 8. Shampoo Your Carpet Carpet is notorious for trapping dust, dirt, and allergens. It’s one of the reasons that most buyers prefer hard surface flooring.12 But if you love your carpet, or you’re not ready to invest in an alternative, make an effort to keep it clean and odor-free. To properly maintain your carpet, you should vacuum it weekly. Experts also recommend a deep shampoo at least every two years.13 Fortunately, this is a cheap and easy DIY project you can knock out in about 20 minutes per room. According to Consumer Reports, you can rent a machine and purchase cleaning fluid and supplies for around $90. With an average return on your investment of 169%, it’s well worth the effort and expense.14 9. Customize Your Closet Real estate professionals estimate that a closet remodel can add $2500 to a home’s selling price. And while a professional renovation can cost upwards of $6000, there are many high-quality DIY closet systems you can customize and install yourself.15 Experts recommend taking a thorough inventory of your wardrobe and accessories before you get started. Make sure frequently-worn pieces are easy to reach, and store seasonal and seldom-used items on high shelves. Place shoe racks near the closet entrance so they are easy to access.16 A little planning can go a long way toward building a closet that you (and your future buyers!) will love. GET A COMPLIMENTARY ANALYSIS OF YOUR PROJECT We’ve been talking averages. But the truth is, the actual impact of a home improvement project will vary depending on your particular home and neighborhood. Before you get started, contact me to schedule a free virtual or in home consultation. I can help you determine which upgrades will offer the greatest return on your effort and investment. Sources: 1. HomeLight - https://www.homelight.com/blog/improve-curb-appeal-landscaping/ 2. National Association of Realtors - https://www.realtor.com/advice/home-improvement/landscape-renovations-that-pay-off/ 3. HouseLogic.com - https://www.houselogic.com/save-money-add-value/add-value-to-your-home/adding-curb-appeal-value-to-home/ 4. Fixr - https://www.fixr.com/blog/2020/01/14/paint-color-trends-in-2020/ 5. T3 Sixty - https://blog.coldwellbanker.com/wp-content/uploads/2018/01/CES2018-Smart-Homes-An-Emerging-Real-Estate-Opportunity.pdf 6. Consumer Reports - https://www.consumerreports.org/smart-home/smart-home-tech-upgrades-to-help-sell-your-house/ 7. American Council for Energy Efficient Economy https://www.aceee.org/sites/default/files/publications/researchreports/a1801.pdf 8. Forbes - https://www.forbes.com/sites/trulia/2016/07/05/10-upgrades-under-1000-that-increase-home-values-2/#47b0d3162e60 9. Insider - https://www.insider.com/home-design-rules-you-should-be-breaking-2020-1 10. Zillow - https://www.zillow.com/sellers-guide/roi-for-bathroom-remodel/ 11. Lowes - https://www.lowes.com/n/how-to/remove-a-bathroom-mirror 12. HomeLight - https://www.homelight.com/blog/what-flooring-increases-home-value/ 13. Angie’s List - https://www.angieslist.com/articles/how-often-should-i-clean-my-carpets.htm 14. HomeLight - https://www.homelight.com/blog/projects-that-increase-home-value/ 15. National Association of Realtors - https://www.nar.realtor/research-and-statistics/research-reports/remodeling-impact 16. EasyClosets - https://www.easyclosets.com/tips-ideas/2016/10/02/how-to-plan-your-walk-in-closet/  Traditionally, spring is one of the busiest times of the year for real estate. However, the coronavirus outbreak—and subsequent stay-at-home orders—led many buyers and sellers to put their moving plans on hold. In April, new listings fell nearly 45%, and sales volume fell 15% compared to last year.1

Fortunately, as restrictions have eased, we’ve seen an uptick in market activity. And economists at Realtor.com expect a rebound in July, August, and September, as fears about the pandemic subside, and buyers return to the market with pent-up demand from a lost spring season.2 But given safety concerns and the current economic climate, is it prudent to jump back into the real estate market? Before you decide, it’s important to consider where the housing market is headed, how it could impact your timeline and ability to buy a home, and your own individual needs and circumstances. WHAT’S AHEAD FOR THE HOUSING MARKET? The economic aftermath of the coronavirus outbreak has been severe. We’ve seen record unemployment numbers, and economists believe the country is headed toward a recession. But people still need a place to live. So what effect will these factors have on the housing market? Home Values Projected to Remain Stable Many Americans recall our last recession and assume we will see another drop in home values. But the 2008 real estate market crash was the cause—not the result—of that downturn. In fact, ATTOM Data Solutions analyzed real estate prices during the last five recessions and found that home prices actually went up in most cases. Only twice (in 1990 and 2008) did prices fall, and in 1990 it was by less than one percent.3 Many economists expect home values to remain relatively steady this time around. And so far, that’s been the case. As of mid-May, the median listing price in the U.S. was up 1.4% from the same period last year.4 Demand for Homes Will Exceed Available Supply There’s been a shortage of affordable homes on the market for years, and the pandemic has further hindered supply. In addition to sellers pulling back, new home starts fell 22% in March.5 In fact, Fannie Mae doesn’t foresee a return to pre-pandemic construction levels before the end of 2021.6 This supply shortage is expected to prop up home prices, despite recessionary pressures. Fannie Mae and the National Association of Realtors predict housing prices will rise slightly this year7, while Zillow expects them to fall between 2-3%.8 Still, that would be a far cry from the double-digit declines that occurred during the last recession.9 Government Intervention Will Help Stabilize the Market Policymakers have been quick to pass legislation aimed at preventing a surge in foreclosures like we saw in 2008. The Coronavirus Aid, Relief, and Economic Security (CARES) Act passed by Congress gives government-backed mortgage holders who were impacted by the pandemic up to a year of reduced or delayed payments.10 The Federal Reserve has also taken measures to help stabilize the housing market, lower borrowing costs, and inject liquidity into the mortgage industry. These steps have led to record-low mortgage rates that should help drive buyer demand and make homeownership more affordable for millions of Americans.11 HOW HAS THE REAL ESTATE PROCESS CHANGED? As the pandemic hit, real estate and mortgage professionals across the country revised their processes to adapt to shifting safety standards and economic realities. While these new ways of conducting business may seem strange at first, keep in mind, military clients, international buyers, and others have utilized many of these methods to buy and sell homes for years. New Safety Procedures The safety of our clients and our team members is our top priority. That’s why we’ve developed a process for buyers and sellers that utilizes technology to minimize personal contact. For our listings, we’re holding online open houses, offering virtual viewings, and conducting walk-through video tours. We’re also using video chat to qualify interested buyers before we book in-person showings. This enables us to promote your property to a broad audience while limiting physical foot traffic to only serious buyers. Likewise, our buyer clients can view properties online and take virtual video tours to minimize the number of homes they step inside. Ready to visit a property in person? We can decrease surface contact by asking the seller to turn on all the lights and open doors and cabinets before your scheduled showing. The majority of our “paperwork” is also digital. In fact, many of the legal and financial documents involved in buying and selling a home went online years ago. You can safely view and eSign contracts from your smartphone or computer. Longer Timelines and Higher Mortgage Standards The real estate process is taking a little longer these days. Both buyers and sellers are more cautious when it comes to viewing and showing homes. And with fewer house hunters and less available inventory, it can take more time to match a buyer with the right property. In a recent survey, 67% of Realtors also reported delays in the closing process. The top reasons were financing and buyer job loss, but appraisals and home inspections are also taking more time due to shifting safety protocol.12 Securing a mortgage may take longer, too. With forbearance requests rising, lenders are getting increasingly conservative when it comes to issuing new loans. Many are raising their standards—requiring higher credit scores and larger down payments. Prepare for greater scrutiny, and build in some extra time to shop around.13 IS IT THE RIGHT TIME FOR ME TO MAKE A MOVE? The reality is, there’s no “one size fits all” answer as to whether it’s a good time to buy or sell a home because everyone’s circumstances are unique. But now that you know the state of the market and what you can expect as you shop for real estate, consider the following questions: Why do you want or need to move? It’s important to consider why you want to move and if your needs may shift over the next year. For example, if you need a larger home for your growing family, your space constraints aren’t likely to go away. In fact, they could be amplified as you spend more time at home. However, if you’re planning a move to be closer to your office, consider whether your commute could change. Some companies are rethinking their office dynamics and may encourage their employees to work remotely on a permanent basis. How urgently do you need to complete your move? If you have a new baby on the way or want to be settled before schools open in the fall, we recommend that you begin aggressively searching as soon as possible. With fewer homes on the market and a lengthier closing process, it’s taking longer than usual for clients to find and purchase a home. However, if your timeline is flexible, you may be well-positioned to score a deal. We’re seeing more highly-incentivized sellers who are willing to negotiate on terms and price. Talk to us about setting up a search so we can keep an eye out for any bargains that pop up. And get pre-qualified for a mortgage now so you’ll be ready to act quickly. If you’re eager to sell this year, now is the time to begin prepping your home for the market. A second wave of infections is predicted for the winter, which could mean another lockdown.14 If you wait, you might miss your window of opportunity. How long do you plan to stay in your new home? The U.S. real estate market has enjoyed steady appreciation since 2012, which made it fairly easy for owners and investors to buy and sell properties for a profit in a short period of time. However, with home values expected to remain relatively flat over the next year, your best bet is to buy a home you can envision yourself keeping for several years. Fortunately, at today’s rock-bottom mortgage rates, you can lock in a low interest rate and start building equity right away. Can you meet today’s higher standards for securing a mortgage? Mortgage lenders are tightening their standards in response to the growing number of mortgage forbearance requests. Many have raised their minimum credit score and downpayment requirements for applicants. Even if you’ve been pre-qualified in the past, you should contact your lender to find out if you meet their new, more stringent standards. Is your income stable? If there’s a good chance you could lose your job, you may be better off waiting to buy a home. The exception would be if you’re planning to downsize. Moving to a less expensive home could allow you to tap into your home equity or cut down on your monthly expenses. WHEN YOU’RE READY TO MOVE—WE’RE READY TO HELP While uncertain market conditions may give pause to some buyers and sellers, they can actually present an opportunity for those who are willing, able, and motivated to make a move. Your average spring season would be flooded with real estate activity. But right now, only motivated players are out in the market. Today’s record-low mortgage rates could give a big boost to your purchasing power. In fact, if you’ve been priced out of the market before, this may be the perfect time to look. If you’re hoping to sell this year, you’ll have fewer listings to compete against in your neighborhood and price range. But you’ll want to act quickly. Economists expect a surge of eager buyers to enter the market in July—so you should start prepping your home now. And keep in mind, a second wave of coronavirus cases could be coming in this winter. Ask yourself how you will feel if you have to face another lockdown in your current home. Let’s schedule a free virtual consultation to discuss your individual needs and circumstances. I can help you assess your options and create a plan that makes you feel both comfortable and confident during these unprecedented times. The above references an opinion and is for informational purposes only. It is not intended to be financial advice. Consult a financial professional for advice regarding your individual needs. Sources: 1. Forbes - https://www.forbes.com/sites/ellenparis/2020/05/08/latest-housing-market-update-from-realtorcom/#20bf7829113e 2. HousingWire - https://www.housingwire.com/articles/realtor-com-housing-market-will-bounce-back-this-year-but-the-rebound-will-be-short-lived/ 3. Curbed - https://www.curbed.com/2019/1/10/18139601/recession-impact-housing-market-interest-rates 4. Realtor.com - https://www.realtor.com/research/weekly-housing-trends-view-data-week-may-9-2020/ 5. Money.com - https://money.com/coronavirus-real-estate-home-prices/ 6. Fannie Mae - https://www.fanniemae.com/resources/file/research/emma/pdf/Housing_Forecast_051320.pdf 7. HousingWire - https://www.housingwire.com/articles/pending-home-sales-tumble-on-covid-19-shock/ 8. HousingWire - https://www.housingwire.com/articles/zillow-predicts-small-home-price-drop-through-rest-of-2020/ 9. Federal Reserve Bank of St. Louis - https://fred.stlouisfed.org/series/CSUSHPINSA 10. Consumer Financial Protection Bureau - https://www.consumerfinance.gov/coronavirus/cares-act-mortgage-forbearance-what-you-need-know/ 11. Bankrate - https://www.bankrate.com/mortgages/federal-reserve-and-mortgage-rates 12. National Association of Realtors - https://www.nar.realtor/sites/default/files/documents/2020-05-11-nar-flash-survey-economic-pulse-05-14-2020.pdf 13. Forbes - https://www.forbes.com/sites/alyyale/2020/04/17/buying-a-home-during-the-pandemic-dont-expect-your-everyday-home-purchase/#fadad3d33b0c 14. Washington Post - https://www.washingtonpost.com/health/2020/04/21/coronavirus-secondwave-cdcdirector/   These days, it seems like everyone’s looking for ways to cut costs and stretch their income further. Fortunately, there are some simple steps you can take to reduce your household expenses without making radical changes to your standard of living. When combined, these small adjustments can add up to significant savings each month. Here are 20 things you can start doing today to lower your bills, secure better deals, and begin working toward your financial goals.

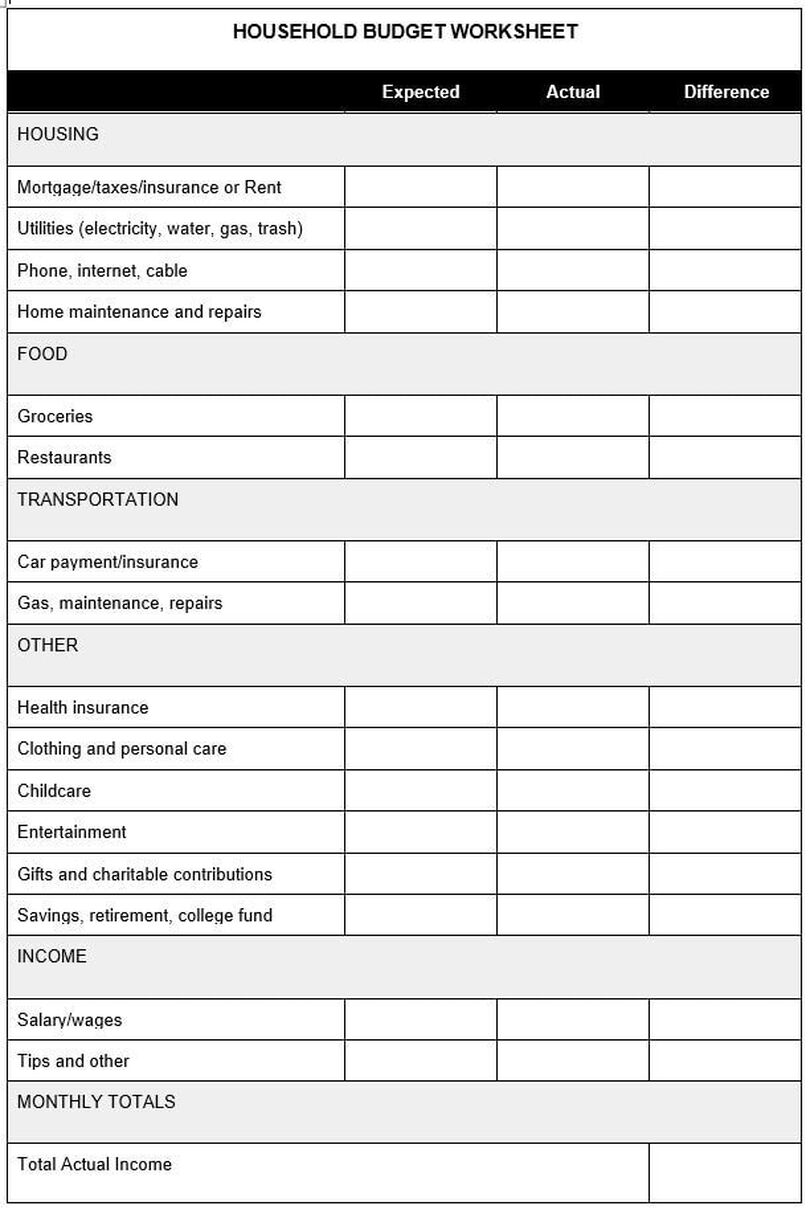

Want more help getting a handle on your finances? Use the budget worksheet below to track income and expenses—and start working towards your financial goals today! Please reach out to me for a downloadable version. WE’RE HERE TO HELP I would love to help you meet your financial goals. Whether you want to refinance your mortgage, save up for a down payment, or simply find lower-cost alternatives for home repairs, maintenance, or utilities, I am happy to provide my insights and referrals. And if you have plans to buy or sell a home this year, we can discuss the steps you should be taking to financially prepare. Contact me today to schedule a free consultation! The above references an opinion and is for informational purposes only. It is not intended to be financial advice. Consult a financial professional for advice regarding your individual needs. Sources:

Since the outbreak of the novel coronavirus (COVID-19), many of us are spending a lot more time at home. We’re all being called upon to avoid public spaces and practice social distancing to help slow the spread of this infectious disease. While it can be understandably challenging, there are ways you can modify your home and your lifestyle to make the best of this difficult situation.